Master Market Structure Analysis: How To Use NetStat to Anticipate Price Moves Through Delta, Gamma, Charm, and Vanna

Market Structure Analysis Introduction

There are two types of SPX 0DTE traders:

- those who only watch price action and get caught off guard when price suddenly breaks through their levels, and

- those who understand the structural forces driving price movement, allowing them to anticipate moves before they happen.

While charts can show you what’s happening, they can’t reveal why price might suddenly accelerate or reverse. That’s where option Greek exposures become critical – they uncover the hidden forces creating powerful market moves.

In this guide, we’ll break down our NetStat (“NET Greek STATus”) tool, which transforms complex Greek forces into clear, actionable trading levels that reveal critical market structure before price movements occur.

Table of Contents

Understanding Market Structure Through Greek Exposures

Think of NetStat as your market structure dashboard – a comprehensive snapshot of how four core option Greeks influence price movement at any point in time:

- Delta tells you who controls price movement in the moment (call or put speculators)

- Charm shows how that control evolves as time passes during the trading day

- Gamma reveals where price movement could suddenly accelerate

- Vanna indicates how volatility changes impact price movement

For example, when a large concentration of out-of-the-money (OTM) calls suddenly becomes in-the-money (ITM), market makers must adjust their hedges quickly, often accelerating price movement. NetStat helps you spot these potential acceleration points before they happen, rather than reacting after the move.

Instead of drowning in complex calculations, NetStat presents this information in a simple table that reveals:

- Who’s really controlling price movement – call or put speculators

- Whether dominant positions are ITM or OTM (indicating how delta might shift as time passes)

- Where the largest concentrations of options exist above and below current price (creating key inflection points)

Understanding this “chess board” of market structure is crucial because it shows both the distribution and concentration of positioning, which directly impacts potential price movement. This insight is especially powerful for SPX 0DTE trading, where these forces play out within a single session.

The Genesis of NetStat

At GammaEdge, we offer 3-D surface models for each Greek (delta, gamma, charm, and vanna). NetStat’s power lies in its ability to distill key information from these complex 3-D models into one snapshot table. While it doesn’t provide all the granular details of the full models, NetStat offers an excellent summary of the four Greeks and key sensitivity points within the market structure.

NetStat is most valuable for understanding how the dominant moneyness (ITM or OTM) above and below spot price influences the options complex. Specifically, NetStat reveals:

- The dominant strike in the Right Hand Plane (RHP) (above spot price) and Left Hand Plane (LHP) (below spot price) for each Greek

- Whether calls or puts are the dominant force above and below spot price

- The moneyness (OTM or ITM) of these forces

This information helps identify whether the market structure provides bullish tailwinds (call dominance) or bearish headwinds (put dominance).

Delta: The Primary Force Behind Price Movement

Delta is the only “first-order” Greek and serves as the primary measurement of risk that market makers hedge. Simply put, delta measures how sensitive your position is to movements in the underlying asset (e.g., SPX).

NetStat helps you identify:

- The dominant strike prices where Delta exposure is largest

- Whether calls or puts control the area above current price

- Whether calls or puts control the area below current price

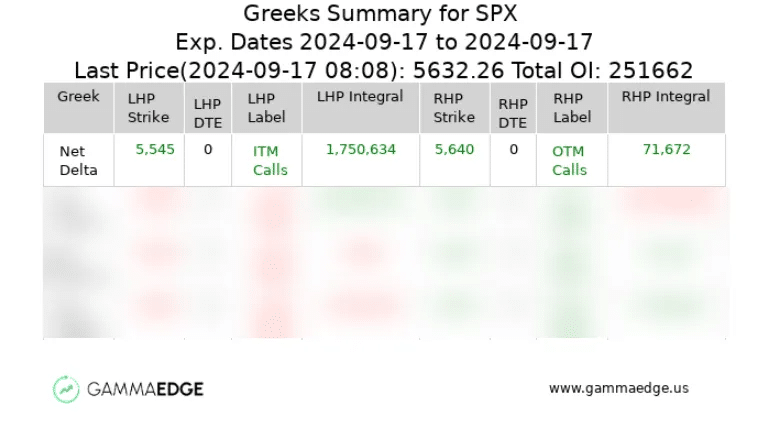

Let’s examine what a NetStat output might tell us about market structure:

Above Spot Price (RHP):

- The key strike is 5640

- The RHP is net-dominant OTM Calls

- The RHP Integral is +71,672 (green), showing overall positive deltas

- If the price moves above 5640, these OTM calls become ITM, potentially accelerating price movement as those deltas shift ITM and into the LHP

Below Spot Price (LHP):

- The key strike is 5545

- The LHP is net-dominant ITM calls

- The LHP Integral is +1,750,634 (green), confirming strong positive deltas

- A call-dominated LHP tells us that puts are not establishing a foothold, which helps maintain bullishness

The big picture? Calls (long deltas) are firmly in control of the structure above and below the current price – a bullish setup. The 5640 strike is particularly important to watch as crossing it from below could trigger accelerated upward movement due to the OTM-to-ITM shift in those calls and the subsequent influence on the Dealer’s hedging.

Charm: How Time Decay Influences Price Movement

Charm is a “second-order” Greek that influences Delta through the passing of time.

As time passes during the trading day, Delta changes even if spot price stays flat or volatility remains constant. This is where Charm comes in. Understanding Charm exposure helps you anticipate:

- How time decay towards expiry affects option positions throughout the session

- Whether this decay creates buying or selling pressure

- Which strikes become more or less important as time passes

It’s important to remember the following:

- ITM options limit their delta to +1 (long calls) or -1 (long puts) as time to expiry decreases

- OTM options decay their delta to 0 as time to expiry decreases (long calls decrease from a positive delta to 0, long puts decrease from a negative delta to 0)

With this in mind, a quick cheat-sheet is the following:

- The LHP contains ITM Calls + OTM Puts – that’s it, there is no other combination possible. If the net of each of these is long, then we have a positive charm value, e.g., the long ITM calls are net limiting to +1 and the long OTM puts are net decaying from a negative value towards 0.

- The RHP contains OTM Calls + ITM Puts – again, this is the only possible combination above spot price. If the net of each of these is long, then we have negative charm value, e.g., the long OTM calls are net decaying to 0 from a positive value and the long ITM puts are limiting towards a negative value of -1.

This is the exact influence of Charm, and we have to remember that this limit or decay component is always present.

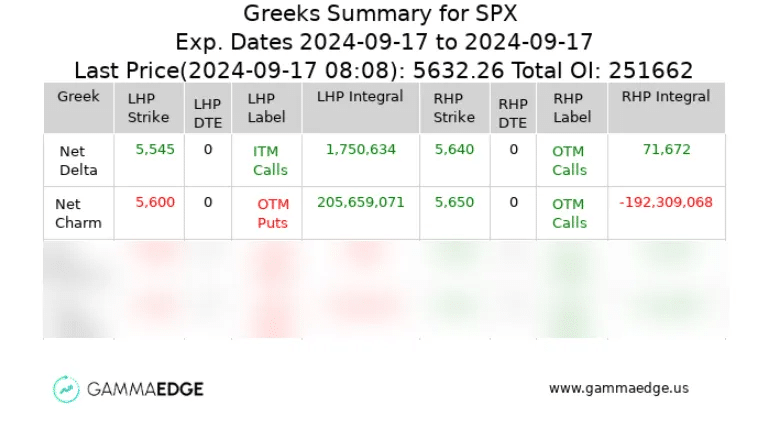

Revisiting our earlier example:

We showed above that for the Net Delta row, ITM Call delta significantly outweighs OTM Put delta activity in the LHP. This is shown by the green LHP Integral value of 1,750,634.

The second row, which is Net Charm, shows that we have a very large dominant strike in the LHP at 5600. We also see that the LHP consists of Net OTM Puts. This may be counter-intuitive: how can the LHP have an ITM Call dominance (Net Delta) but have an OTM Put dominance (Net Charm)?

The answer has to do with moneyness. Once a long ITM call has hit Delta = +1, it has no more charm to give. Deep ITM calls fall into this category – they have limited to Delta = +1. Charm in this case, where the option Delta = +1, is zero – there is no further change in delta due to time for that option.

In this case, because the LHP contains both ITM Calls and OTM Puts, we have a situation where the OTM Puts are decaying towards 0 from a negative value, and their decay – in aggregate, is creating more positive charm flow than the ITM Calls. This is why the LHP label shows “OTM Puts” – the ITM Calls have already limited to +1, and all that is left are decaying OTM Puts.

The OTM Puts in the Net Charm LHP will, by definition, decay as the day progresses towards expiry. We would expect, with a steady price, that the 205,659, 071 value shown in the LHP Integral will drop.

The RHP Net Charm side can be considered just like we did for the LHP side. Here, we have dominant OTM Calls that are decaying, hence, the -192,309,068 (red) negative value.

BOTH of the Net Charm components, the LHP and the RHP, are comprised of Net OTM options, so they both will get smaller as the day progresses. On the other hand, if one of these was dominant with an ITM option (ITM Calls in the LHP or ITM Puts in the RHP), we expect Net Charm to increase for that ITM side as we move towards expiry.

In the scenario above, assuming all else equal:

- LHP Charm integral will decrease throughout the session but maintain a positive delta contribution.

- RHP Charm integral will also decrease throughout the session, maintaining a negative delta contribution.

- The NET of these two Charm Integrals will favor support from the LHP, but this support gets smaller the closer we get to expiry.

The NET of the LHP Charm Integral and RHP Charm Integral is often where we see price fail to decline (LHP Net Charm > RHP Net Charm) or we see price fail to advance (RHP Net Charm > LHP Net Charm).

In our example above, the balance goes towards some support, but because these are DECAYING, the support is getting weaker and weaker as the day progresses.

Do you see how Delta and Charm interrelate and why they’re crucial to understanding?

Here’s a video further explaining Charm influences in our trading.

Gamma: The Price Movement Accelerator

Gamma is another second-order Greek that influences Delta through a change in spot price.

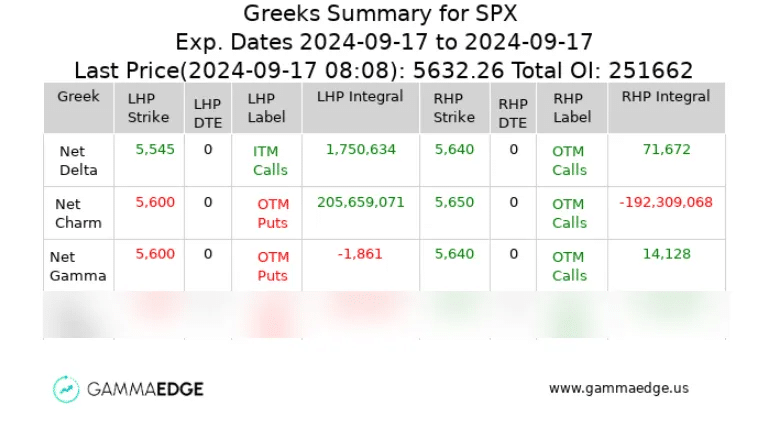

When price moves through key Gamma strikes, Delta can change rapidly – think of Gamma as your market accelerator. Through NetStat, we can identify these potential acceleration points:

- Above Spot Price (RHP): Focus on the largest Gamma strikes where price movement could accelerate to the upside

- Below Spot Price (LHP): Watch for key Gamma strikes that could trigger quick moves lower

Using the same example above, large Gamma sits at strike 5640 above spot price. If price starts moving upward through this level, we could see an acceleration higher as:

- The large concentration of OTM calls at 5640 move ITM

- OTM Call Deltas rapidly shift from less than 0.5 to greater than 0.5 (and growing to +1)

- Dealers suddenly become much shorter, and their hedging (buying to move neutral) can amplify the upward move

It’s worth noting in the NetStat table above that there is also a large Gamma strike down at 5600. You’ll also note that the current spot price of 5632 is closer to the upper Gamma strike of 5640 than it is the lower Gamma strike of 5600. Gamma is sensitive to spot price, and the closer the spot price is to a Gamma strike, the larger the gamma at that strike.

If the price were to drop towards 5600, we would see the put-dominant 5600 strike grow in negative gamma and the upper 5640 strike drop in positive gamma.

This is how it works: Gamma has a magnifying impact on the strikes around it, which is usually important to your trading and understanding of market structure analysis.

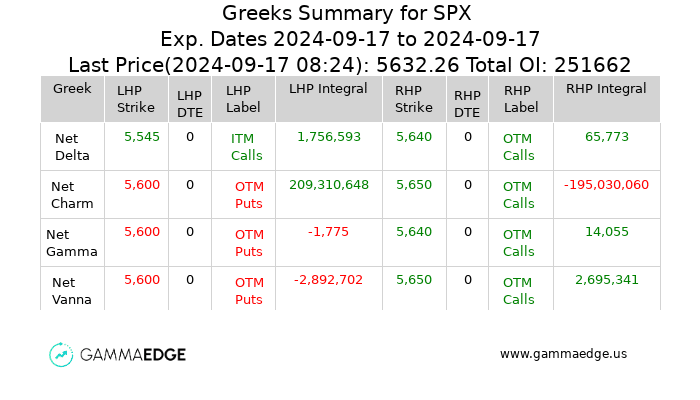

Vanna: The Volatility Impact on Market Structure

Vanna is the last second-order Greek that influences Delta through a change in volatility.

While Gamma shows how Delta changes with price movement and Charm shows how Delta changes with time, Vanna reveals how Delta changes with volatility.

The NetStat table above gives us a view of Vanna’s influence on Delta. As price falls towards the 5600 strike, we would expect the LHP Integral to grow in magnitude and simultaneously, we’d see a drop in the RHP integral as we moved away lower from 5650.

Like Charm, the integral balance of Vanna is often important. The NetStat table allows us to mentally sum the LHP and RHP integrals together, and as shown, there is a net negative impact on Delta. At the current volatility levels, deltas are being removed from the complex, making the overall complex shorter and all-things-equal, slightly tilting the tables more bearish.

You probably see something in the NetStat table which is different from the Charm setup: Vanna is positive in the RHP with OTM Calls and ITM Puts. This is the exact opposite of Charm and can lead to some unique opportunities.

Specifically, we want to watch for the following:

- VIX is elevated (>20)

- There’s potential for volatility contraction

- We start to see the RHP Integral values for Vanna greater than the LHP Integral values for Vanna

Under these conditions, think of Vanna like a coiled spring – when volatility is high and starts to contract, there is often a simultaneous move in prices to higher levels. We think the mechanics of what is happening is powerful and can be used to develop a short-covering thesis. Here’s what happens during this set of circumstances:

- OTM puts rapidly lose value due to price moving upward

- When the market starts to rally, volatility often falls resulting in a lower implied volatility (IV) of the option, reducing its extrinsic value

- Traders often close these decaying OTM Put positions due to the loss of this extrinsic value

- This removal of negative delta can create upward pressure by making “the book” longer, which then…

- Forces Dealers to become shorter and who respond by buying to hedge flat

- Market participants see this rapid move upward and they continue to close OTM Puts as well as start to open OTM calls, with both of these actions fueling the Vanna “short covering” rally

The NetStat tool, in combination with our VolM tool (intraday volume analysis), can help you identify the potential for a Vanna “short covering” rally.

Here’s a video further breaking down the importance of Vanna’s impact.

Practical Application of NetStat in Trading

Remember that Delta is the foundation – Charm, Gamma, and Vanna influence Delta, but it all starts with market participants opening and closing contracts, which directly impacts Delta.

We recommend starting your trading day with NetStat:

- Check Delta dominance first

- Who’s winning (call or put speculators) above and below spot price?

- What’s the moneyness of these positions (OTM or ITM)?

- Where are the largest strikes that could influence price?

- Look for Charm influence

- Will time decay help or hurt your positions today?

- How will the balance of Charm Integrals shift as the day progresses?

- Identify key Gamma strikes

- Where might price accelerate?

- Which strikes could trigger significant hedging activity?

- Consider Vanna (especially if VIX is high)

- Could volatility contraction create upward pressure?

- Are conditions right for a potential short-covering rally?

Pro Tip: NetStat provides the structural framework of the market, showing what COULD happen based on Greek influences and price movements. Combine this with real-time tools to track what’s actually occurring in the market for a comprehensive view of market dynamics.

Common Mistakes To Avoid With NetStat In Your Market Structure Analysis

- Don’t Treat NetStat Levels Like Traditional Support/Resistance

- These are sensitivity points, not exact turning points

- Price can and will trade through them

- Focus on potential acceleration or reversal when levels are crossed

- Remember Market Context Matters

- Are Greeks active enough to significantly influence price?

- Is there enough Gamma in motion?

- Is volatility working in your favor?

- Time’s Constant Influence

- Time decay is always in motion

- Consider what part of the trading day you’re in

- Greeks change more rapidly toward the end of the day than at the beginning

- Never Focus on One Greek Alone

- Delta, Gamma, Charm, and Vanna work together

- Look for confluence between readings

- Consider how they might interact as conditions change

Bringing It All Together: NetStat as Your Market Structure Analysis GPS

Trading without understanding market structure is like boxing with a blindfold – you might land some punches, but you’re missing crucial information about your opponent’s position.

NetStat removes that blindfold, showing you:

- Where the biggest market participants are positioned

- How their positions might influence price movement

- When price is most likely to accelerate or reverse

- Which Greeks are most influential at any given time

Remember: Every trading day is a battle between call and put speculators. NetStat lets you see who’s winning that battle and if their advantage is growing or shrinking – putting you on the right side of structural moves before they happen.

Ready to Master Market Structure Analysis Through The Greeks?

Want to learn more about using NetStat and Greek analysis to improve your trading decisions? Our flagship education course, The GammaEdge Framework, walks you through our entire trading methodology, fully unlocking the power of options market analysis for your trading toolkit.

You’ll discover:

- How to interpret Delta, Gamma, Charm, and Vanna readings

- Which Greek exposures matter most in different market conditions

- How to identify key sensitivity points for entries and exits

- And much more…

Note: The examples shown in this article are from past dates and don’t reflect current market conditions. Be sure to analyze current data for your trading decisions.

We train traders to simplify the options markets with our industry leading data, tools, and education to achieve profitability.

Services

Quick Links

Get In Touch

email: contactus@gammaedge.us